The gap between Liverpool

and Manchester United can be measured in more than just league points. The

total annual gap between the two clubs in terms of revenues generated now sits

at a very concerning £148m per year. The chart below shows how this is broken

down:

Source:

Deloittes Football Money League 2010/11

Here are the same numbers

broken down by the actual revenue gap between the two clubs for each sector:

A large part of the gap in

TV revenue can be closed by Liverpool’s actions on the pitch. For example, £30m

in TV revenue would be immediately generated through participation in the

Champions League. This scenario would also mean a higher merit payment from The

Premier League (c. £6m) and more lucrative gate receipts and commercial

sponsorship opportunities (up to £4m).

The £26m commercial gap

could be partially closed by selling naming rights for the existing Anfield

stadium. Whilst this would not generate anywhere near the £400m paid by the Abu

Dhabi government for the Etihad stadium, it is not inconceivable that it could

bring in an additional £15m per season.

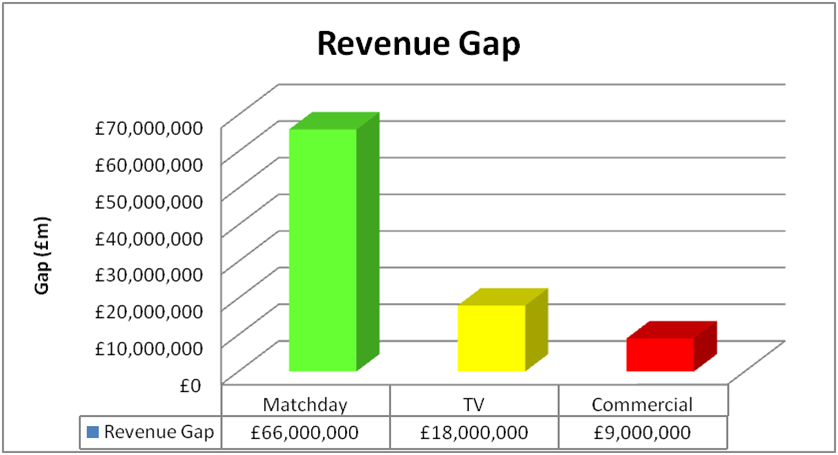

Here is how the revenue gap

between Liverpool and Manchester United would look if we incorporate the £55m

of increased income detailed above:

Clearly, even with success

on the pitch there is still a very significant gap between the two clubs. The

majority of this gap comes from the difference in match day revenue. Even with

Champions League qualification, the match day revenue gap would stand at £66m

per year. Here is a breakdown of this huge difference:

Source: Swiss Ramble

This revenue gap is a huge

problem for Liverpool. From 2013/14, the FFP rules will put severe restrictions

on a club’s ability to invest over and above its annual income. Even if Liverpool

manage to qualify for the Champions League each year, the £93m revenue gap Manchester

United will command will mean that they can invest far more heavily in squad

improvements. The doomsday scenario for Liverpool is that United’s superiority

off the field will inevitably be matched with more success on it, as the

quality of both squads drifts further apart.

United’s Achilles Heel

There is another aspect to

the FFP rules which does not sit as comfortably in United’s favour: that of club

debt. The following chart shows the sheer scale of United’s debt and the

financial burden it puts on them each season. Here is a breakdown of their

actual profit performance last year:

Source: Swiss Ramble

Any operating profits United

make are massively reduced by their need to service the £540m acquisition debt.

In 2011 alone, the interest payable was a whopping £43.5m. The net effect of

this in terms of FFP is that United will have a break even spend allowance of £45m

per year. However, given that the last Liverpool FC accounts available show a

£2.3m loss before interest, and the general consensus that FSG will not spend more

than they earn, this total is highly likely to be considerably more than

Liverpool’s available spend. That is, of course, unless Liverpool’s revenue

streams are significantly increased.

Put simply, in order to operate

on a par with United off the pitch, Liverpool must get back into the Champions

League and get the right financial model in place for a new stadium.

Given how fundamental a new

stadium is to Liverpool’s finances, why is there not already a spade in the ground?

The answer to this question

comes through the key words ‘right financial model’. FSG are reportedly looking

to generate £150m of the estimated £300m cost through up front sponsorship

deals. Should they pull this off, the cost to service the additional £150m

would be somewhere in the region of £10m per year. This cost would be offset by

an additional £1.2m per game in match day revenue (Based on £47 per head) which

would bring in close to £35m per year.

There are lots of risks

attached to this financial model. If FSG are unable to secure the funding up

front, the debt servicing costs could double. Another risk factor comes

from the possibility that Liverpool will fail to fill the stadium or attract

corporate guests, leading to the revenue per head being significantly reduced. This

is a very real possibility, given that the Isla Gladstone corporate facility

was only half full during the last days of the Hodgson era. Yet another risk is that there could be short term cash flow issues affecting Liverpool’s

ability to compete in the transfer market and therefore the league.

However, taking everything into account, there is absolutely no alternative for FSG: They must find that right financial model for a new stadium, and find it now.

However, taking everything into account, there is absolutely no alternative for FSG: They must find that right financial model for a new stadium, and find it now.

The consequences of building

works not starting in the immediate future are almost too much to bear.

Follow Me on Twitter: www.twitter.com/joescouse_lfc

Note: The main source for

the Premier League finances in this article is the exceptional www.swissramble.blogspot.co.uk.

Interesting but you only talk about revenue and debts. How does running costs stack up between the two clubs?

ReplyDelete@bumbling-idiot

ReplyDeleteExtensive info on LFC here: http://swissramble.blogspot.co.uk/search/label/Liverpool

And on Man U here: http://swissramble.blogspot.co.uk/search/label/Manchester%20United

Also the commercial revenue gap will be partially closed by the Warrior deal (25 vs 12m). That will close half the commercial revenue gap.

ReplyDeleteActually, LFCs commercial revenue is quite surprising given our performance over the past few years.

Getting back to CL and getting the stadium deal done are critical to the club's future.

maximum investment for the new stadium can be achieved only if we qualify for the champions league.

ReplyDeleteI think the owners are waiting for this to happen before selling the naming rights of the new stadium.

Very good article. I don't think FSG will invest in a new stadium right away. CL football will be their priority coz unless we have CL football, sponsors will not pay us top money. Let's hope we're in the CL in the 2013-14 season. YNWA.

ReplyDelete